What Does FICO Stand For? Decoding The Credit Score That Rules Your Financial Life

Have you ever found yourself staring at a loan application or a rental agreement, only to be asked for your FICO score? You're not alone. Millions of people have heard the term, but the fundamental question remains: what does FICO stand for? It’s more than just a three-letter acronym on a financial document; it’s a powerful number that can open doors or build walls around your economic future. Understanding its origins, mechanics, and impact is not just financial literacy—it’s a essential life skill in today’s credit-driven world. This guide will pull back the curtain on the entity behind the score, transforming confusion into clarity and empowering you to take control of your financial narrative.

The term "FICO" is ubiquitous in personal finance, yet its meaning is often shrouded in mystery for the average consumer. It’s not a government agency, nor is it your bank. It’s the name of a pioneering analytics company whose creation has become the universal language of creditworthiness. When you grasp what FICO stands for and how its scores function, you move from being a passive subject of credit evaluation to an active participant in your financial health. This article will journey from the company's 1950s inception to the modern-day strategies you can employ, providing a comprehensive roadmap to one of the most important numbers in your life.

The Origins: Fair Isaac Corporation, The Company Behind the Score

To answer what does FICO stand for definitively, we must travel back to its roots. FICO is an acronym for Fair Isaac Corporation, the name of the company founded in 1956 by two brilliant engineers, Bill Fair and Earl Isaac. Their mission was revolutionary for its time: to apply data analytics and statistical modeling to the then-nascent world of consumer credit. Before their work, lending decisions were often made subjectively by individual bankers, leading to inconsistencies and potential biases. Fair and Isaac envisioned a system that could predict credit risk objectively and consistently, using the emerging power of computing.

- The Untold Story Of Mai Yoneyamas Sex Scandal Leaked Evidence Surfaces

- Joseph James Deangelo

- Pineapplebrat Nudes

The company’s early years were spent developing the first automated credit scoring systems, which were initially sold to lenders. Their breakthrough was the creation of a mathematical model that could analyze a borrower’s credit history and generate a single, predictive number. This number, the FICO Score, was first introduced to lenders in 1989 and was later made available to consumers in 1995. Over the decades, Fair Isaac Corporation (which officially changed its ticker symbol to FICO in 2013) has evolved from a niche analytics firm into a global standard-setter. Today, it is a publicly-traded company (NASDAQ: FICO) whose scores are used by over 90% of top U.S. lenders, making it the undisputed heavyweight in credit risk assessment.

The Founders: Bill Fair and Earl Isaac

While the company bears their names, the founders' personal stories are less commonly told. Bill Fair was a mechanical engineer with a knack for statistics, while Earl Isaac was a mathematician and electrical engineer. Their partnership was built on a shared belief that credit could be managed scientifically. They didn't just create a product; they established an entire industry. Their legacy is a double-edged sword: a tool that enables efficient markets and responsible lending, but also a system that requires consumers to understand and navigate its complexities to thrive.

What Exactly Is a FICO Score?

Now that we know the "FICO" in FICO Score, let's define the score itself. A FICO Score is a three-digit number, typically ranging from 300 to 850, that summarizes your creditworthiness based on the information in your credit report from the three major credit bureaus (Experian, Equifax, and TransUnion). Think of it as a grade for your financial responsibility, but one that is constantly recalculated as your credit behavior changes. It is not a measure of your wealth, income, or character; it is a purely statistical prediction of your likelihood to repay a debt on time, as determined by the algorithm created by Fair Isaac Corporation.

- James Broderick

- Facebook Poking Exposed How It Leads To Nude Photos And Hidden Affairs

- Mikayla Campino Leak

Lenders use this score as a primary filter in their decision-making process. A higher score signals lower risk, making you more attractive to lenders. This translates directly into higher approval odds for loans and credit cards, and crucially, lower interest rates. For example, on a 30-year fixed mortgage, the difference between a FICO Score of 680 and 780 can mean an interest rate difference of 0.5% to 1% or more. Over the life of a loan, this can amount to tens of thousands of dollars in saved interest. The score’s influence extends beyond lending; it can affect insurance premiums, utility deposits, and even employment opportunities in some states.

How Is It Different from a Credit Report?

A common point of confusion is the distinction between a FICO Score and a credit report. Your credit report is the raw data—a detailed history of your credit accounts, payment records, inquiries, and public records. It’s like a comprehensive financial transcript. The FICO Score is the distilled analysis of that data, a single number derived from the report’s information using a proprietary formula. You have three credit reports (one from each bureau), and you can have multiple FICO Scores because the company generates different versions of the model, and each bureau’s data may vary slightly.

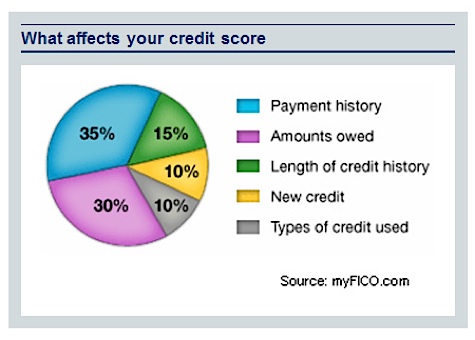

The Five Pillars: How Your FICO Score is Calculated

The magic—and the power—of the FICO Score lies in its weighted factors. The model breaks down your credit report information into five key categories, each with a specific percentage of influence on the final score. Understanding these pillars is the single most important step in managing your credit proactively.

- Payment History (35%): This is the heavyweight champion. It tracks your record of on-time payments across all credit accounts—credit cards, mortgages, auto loans, etc. A single late payment can cause a significant drop, especially if it’s recent or severe (90+ days late). Bankruptcies, foreclosures, and collections also fall here and can devastate your score for years.

- Amounts Owed (30%): Also called credit utilization, this measures how much of your available credit you are using. It’s calculated per card and overall. Keeping your credit card balances below 30% of your limits is a critical rule of thumb, though top scorers often stay under 10%. High utilization suggests you may be over-reliant on credit.

- Length of Credit History (15%): This considers the average age of all your accounts and the age of your oldest account. A longer, stable credit history is a positive. Closing old accounts can hurt this factor by reducing your average age and total available credit.

- Credit Mix (10%): FICO likes to see a diverse portfolio of credit types, such as revolving credit (credit cards) and installment credit (mortgages, auto loans, student loans). You don’t need every type, but a healthy mix shows you can manage different debt structures.

- New Credit (10%): This factor looks at recent applications for new credit (hard inquiries) and the number of newly opened accounts. Multiple inquiries in a short period can signal financial distress or "shopping" for credit, which can lower your score. However, rate-shopping inquiries for a mortgage, auto, or student loan within a 14-45 day window are typically counted as one inquiry.

Practical Example: The 30% Utilization Rule

Let’s make this tangible. Imagine you have two credit cards:

- Card A: $5,000 limit, $1,000 balance (20% utilization)

- Card B: $2,000 limit, $1,500 balance (75% utilization)

Your overall utilization is ($1,000 + $1,500) / ($5,000 + $2,000) = $2,500 / $7,000 ≈ 36%. This is above the recommended 30% threshold and is likely dragging down your score. A simple strategy is to pay down the balance on Card B first to bring its utilization down, which will improve your overall ratio and your score.

The FICO Score Family: It’s Not Just One Number

A critical nuance in answering what does FICO stand for is recognizing that there isn't just one "FICO Score." Fair Isaac Corporation has developed multiple score versions tailored to different industries and risk assessments. The most commonly referenced is the FICO Score 8, which is widely used for general credit card and lending decisions. However, newer versions like FICO Score 9 and FICO Score 10 incorporate trended data (how your balances and payments change over time) and have different treatments for things like medical collections.

More importantly, there are industry-specific scores:

- FICO Auto Score: Used primarily for auto loans.

- FICO Bankcard Score: Used for credit card approvals.

- FICO Mortgage Score: Used for home loans.

These versions place different weights on the five factors to better predict risk for that specific product. For instance, a lender might pull your FICO Score 2 for a mortgage application, while a credit card company uses FICO Score 8. This is why your score can vary slightly depending on where it’s pulled from and for what purpose.

Beyond FICO: The Role of VantageScore

While FICO dominates, it’s not the only player. VantageScore is a competing credit scoring model created jointly by the three major credit bureaus. Its most recent models, VantageScore 3.0 and 4.0, also range from 300-850 and are used by many lenders, particularly in the subprime space, and by many free credit score services (like Credit Karma). Key differences include:

- Inclusion of Alternative Data: VantageScore 4.0 can incorporate utility payments, telecom bills, and rental history (if reported) to help "credit invisible" consumers build a score.

- Different Inquiries Policy: VantageScore counts all hard inquiries for the same loan type within a 14-day window as one, similar to FICO’s mortgage-shopping policy but applied more broadly.

- Lower Minimum Scoring Threshold: VantageScore can generate a score with just one month of credit history and one account reported in the last 24 months, whereas FICO typically requires at least six months of history and one account reported in the last six months.

For the average consumer, the takeaway is: don't obsess over a single number. Focus on the fundamentals—pay on time, keep utilization low—which will improve your scores across all models.

Gaining Access: How to Find Your Official FICO Score

For years, FICO Scores were a closely guarded secret between lenders and bureaus. But thanks to regulations and consumer demand, access is now much easier. However, it’s crucial to know where to look.

- Direct from myFICO.com: This is the official source. You can purchase your FICO Score 8 based on each credit bureau’s data, along with your full credit report and additional score versions (like mortgage or auto scores). This is the most accurate and comprehensive option, but it’s a paid service.

- Through Lenders and Credit Card Issuers: Many major banks and credit card companies now provide free FICO Scores as a cardholder benefit. They typically update monthly and are a fantastic, no-cost way to monitor your score. Check your online account portal or statements.

- Free Credit Score Services: Websites and apps like Credit Karma (VantageScore), WalletHub (VantageScore), and AnnualCreditReport.com (official free annual credit reports, but not scores) are useful for monitoring. Always check which scoring model is being provided to avoid confusion.

- Credit Unions and Community Banks: Many smaller institutions also offer free FICO Scores to their members as a value-add.

Important: When checking your own score, ensure it’s a "soft inquiry," which has no negative impact. Only "hard inquiries" from actual credit applications affect your score.

Taking Control: Actionable Steps to Improve Your FICO Score

Understanding what FICO stands for is useless without action. Here is a prioritized, actionable plan based on the five-factor model:

- Automate On-Time Payments: Set up autopay for at least the minimum due on every account. Payment history is 35% of your score—this is non-negotiable.

- Aggressively Reduce Credit Card Balances: Focus on high-utilization cards first. Paying down a $500 balance on a $1,000 limit card (from 50% to 0%) will likely boost your score more than paying down a $2,000 balance on a $10,000 limit card (from 20% to 15%).

- Keep Old Accounts Open: Don’t cancel that old credit card you rarely use, unless it has an annual fee. Its age and its credit limit contribute positively to your score.

- Limit New Credit Applications: Only apply for new credit when absolutely necessary. Each hard inquiry can knock a few points off and stays on your report for two years.

- Diversify Strategically: If you only have credit cards, consider a credit-builder loan or a small personal loan in the future to add an installment account to your mix, but only if it makes financial sense.

- Dispute Inaccuracies: Regularly review your credit reports from AnnualCreditReport.com. Dispute any errors (late payments you didn’t make, accounts you don’t recognize) directly with the credit bureau. Correcting a major error can provide a quick score boost.

Frequently Asked Questions (FAQs)

Q: Does checking my FICO Score hurt it?

A: No. Checking your own score is a soft inquiry and has zero impact. Only when a potential lender checks it for a credit decision (a "hard inquiry") does it potentially lower your score slightly.

Q: How often does my FICO Score update?

A: Your score updates whenever your credit report data changes. Since creditors report to the bureaus at different times (usually monthly), your score can fluctuate frequently. Major changes like paying down a large balance or a late payment posting will trigger an update.

Q: What is a "good" FICO Score?

A: While lenders have their own criteria, general ranges are:

- 800-850: Exceptional

- 740-799: Very Good

- 670-739: Good

- 580-669: Fair

- 300-579: Poor

Aim for at least the "Good" range to qualify for the best rates.

Q: Can I get a perfect 850 FICO Score?

A: Yes, but it’s extremely rare and requires a decades-long, flawless credit history with a perfect mix of accounts and zero utilization. For practical purposes, a score of 760+ will get you the best rates available.

Q: Is my FICO Score the same at all three credit bureaus?

A: Not necessarily. Because each bureau may have slightly different information (creditors don’t always report to all three), your score can vary by 20-30 points between them. Lenders may pull from any one of them, or a consolidated version.

Conclusion: Your Score, Your Power

So, what does FICO stand for? It stands for Fair Isaac Corporation, the company that invented modern credit scoring. But more importantly, it stands for opportunity, cost, and access. Your FICO Score is a dynamic reflection of your financial behavior, a key that can unlock favorable terms for a home, a car, or a business, or a barrier that makes life more expensive. It is not a permanent judgment but a mutable metric you can influence with knowledge and discipline.

The power has shifted from the lender’s subjective desk to your hands, armed with transparency. By understanding the history of Fair Isaac Corporation, the anatomy of the score itself, and the concrete steps to improve it, you demystify the system. You move from asking "what does FICO stand for?" to commanding "this is what my FICO score means for my future." Start today: check your score for free through your bank, analyze your credit reports for errors, and implement one strategy from the five pillars. Your financial life is not defined by a single number, but mastering this number is one of the smartest moves you can make for a stable and prosperous future.