Understanding ACHMA VISB Bill Payments: A Complete Guide

Have you ever encountered a charge on your credit card statement labeled ACHMA VISB and wondered what it means? You're not alone. Many consumers are puzzled by this cryptic billing identifier that appears on their statements. This comprehensive guide will demystify ACHMA VISB bill payments, explain why they appear on your account, and provide you with everything you need to know about managing these transactions effectively.

What is ACHMA VISB?

ACHMA VISB stands for ACH (Automated Clearing House) Merchant Authorization and VISB (typically referring to Visa billing). This payment processing code represents a specific type of electronic transaction that occurs when you make purchases or payments using your Visa card through ACH processing networks. These transactions are commonly associated with Walmart and Sam's Club purchases, as these retail giants use this billing identifier for certain types of transactions processed through their payment systems.

When you see ACHMA VISB on your statement, it indicates that the transaction was processed through an automated clearing house network rather than traditional credit card processing. This method is often used for recurring payments, subscription services, and certain retail transactions where ACH processing offers advantages in terms of processing fees and settlement times.

- Kaliknockers

- Exclusive Leak The Yorkipoos Dark Secret That Breeders Dont Want You To Know

- Peitners Shocking Leak What Theyre Hiding From You

How ACHMA VISB Transactions Work

Understanding the mechanics behind ACHMA VISB bill payments can help you better manage your finances and recognize legitimate charges. These transactions operate through a sophisticated network of financial institutions and payment processors that facilitate electronic fund transfers between merchants and consumers.

The ACH Network Explained

The Automated Clearing House (ACH) network is a secure electronic system that processes financial transactions in batches. Unlike real-time credit card authorizations, ACH transactions are processed in large groups at scheduled intervals throughout the day. This batching process allows for more efficient processing but can result in slight delays between when you make a purchase and when it appears on your statement.

When you make a purchase at a participating retailer or authorize a recurring payment, the merchant's payment processor initiates an ACH transaction through the network. The transaction includes your account information, the amount to be debited, and the merchant's identification details. The ACH network then routes this information to your bank or credit card issuer for processing and settlement.

- Demetrius Bell

- Dancing Cat

- Starzs Ghislaine Maxwell Episodes Leaked Shocking Nude Photos Sex Tapes Exposed

Visa's Role in ACHMA VISB Transactions

The VISB component of ACHMA VISB refers to Visa's involvement in these transactions. While ACH is primarily associated with direct bank transfers, Visa has integrated its payment processing capabilities with ACH networks to provide additional security features and fraud protection. This integration allows merchants to benefit from ACH's cost-effectiveness while maintaining the security standards associated with major credit card networks.

Visa's participation also means that these transactions are subject to the same dispute resolution procedures and consumer protections that apply to other Visa transactions. If you need to dispute an ACHMA VISB charge, you can typically do so through your card issuer's standard dispute process.

Common Scenarios for ACHMA VISB Charges

ACHMA VISB bill payments appear in various contexts, and understanding these scenarios can help you identify legitimate charges versus potential fraudulent activity. Here are the most common situations where you might encounter these transactions:

Retail Purchases at Major Stores

Many large retailers, particularly Walmart and Sam's Club, use ACHMA VISB processing for certain types of transactions. This includes in-store purchases made with credit cards, online orders, and recurring subscription services like Walmart+ or Sam's Club Plus memberships. The use of ACH processing allows these retailers to reduce payment processing fees while maintaining efficient transaction processing.

If you've recently shopped at Walmart or Sam's Club and see an ACHMA VISB charge, it's likely related to your purchase. These charges may appear on your statement within 1-3 business days after your transaction, depending on when the ACH batch processing occurs.

Subscription Services and Recurring Payments

Many subscription-based services utilize ACHMA VISB processing for recurring billing. This includes streaming services, software subscriptions, membership programs, and other services that charge customers on a regular basis. The ACH network's ability to process scheduled payments makes it ideal for subscription billing models.

When you sign up for a subscription service that uses ACHMA VISB processing, you may notice the charges appearing consistently on your statement. These transactions typically include additional information in the description field that can help you identify the specific service or merchant associated with the charge.

Utility and Service Bill Payments

Some utility companies, telecommunications providers, and other service-based businesses use ACHMA VISB processing for customer payments. This can include electricity bills, internet service charges, phone bills, and other regular service payments. The ACH network's reliability and cost-effectiveness make it attractive for businesses that process large volumes of recurring payments.

If you've authorized automatic payments for utility bills or service subscriptions, you may see ACHMA VISB charges on your statement corresponding to these payments. These transactions typically include the merchant's name or a reference number that can help you identify the specific service being paid.

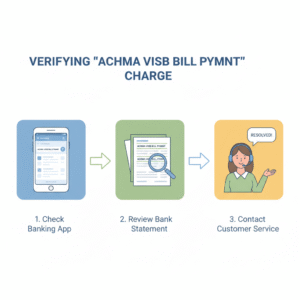

How to Identify Legitimate ACHMA VISB Charges

With the prevalence of electronic transactions, it's essential to be able to distinguish between legitimate ACHMA VISB bill payments and potentially fraudulent charges. Here are several strategies to help you verify the authenticity of these transactions:

Check Your Recent Purchase History

The first step in identifying legitimate ACHMA VISB charges is to review your recent purchase history. Think about where you've shopped in the past few days or weeks, particularly at retailers known to use this processing method. If you've made purchases at Walmart, Sam's Club, or other major retailers, there's a good chance the ACHMA VISB charge is related to those transactions.

Consider the timing of the charge as well. ACH transactions typically take 1-3 business days to process and appear on your statement. If you see an ACHMA VISB charge that corresponds to a purchase made several days ago, it's likely legitimate. However, if the timing doesn't match your purchase history, you may need to investigate further.

Look for Additional Transaction Details

Many ACHMA VISB transactions include additional information in the transaction description that can help you identify the merchant or service associated with the charge. This might include the merchant's name, a reference number, or other identifying information. Take the time to read the complete transaction description carefully.

If the description includes information that matches your recent activities or known subscriptions, it's likely a legitimate charge. However, if the description is vague or doesn't correspond to any of your known transactions, you should contact your card issuer to investigate further.

Contact the Merchant Directly

If you're unable to identify a charge through your purchase history or transaction details, consider contacting the merchant directly. Many businesses that use ACHMA VISB processing have customer service departments that can help you verify charges and provide additional information about their billing practices.

When contacting the merchant, be prepared to provide them with the transaction details from your statement, including the amount, date, and any reference numbers included in the description. This information can help them locate the specific transaction in their system and provide you with clarification.

Managing and Disputing ACHMA VISB Charges

Even with careful monitoring of your transactions, you may occasionally need to manage or dispute ACHMA VISB bill payments. Understanding the proper procedures for handling these situations can save you time and frustration.

Reviewing Your Statements Regularly

The key to managing ACHMA VISB charges effectively is to review your credit card statements regularly and thoroughly. Make it a habit to check your statements at least once a week, looking for any unfamiliar charges or discrepancies. Pay particular attention to the transaction descriptions and amounts, comparing them to your purchase receipts and records.

Regular statement review allows you to catch any unauthorized or incorrect charges early, making the dispute process much simpler. Most card issuers have specific time limits for disputing charges, so prompt identification is crucial for successful resolution.

The Dispute Process for ACHMA VISB Charges

If you identify a charge that you believe is incorrect or unauthorized, the dispute process for ACHMA VISB transactions is similar to that for other credit card charges. Start by contacting your card issuer's customer service department, either by phone or through their online banking portal. Be prepared to provide detailed information about the charge, including the transaction date, amount, and your reasons for disputing it.

Your card issuer will typically initiate an investigation, which may involve contacting the merchant and reviewing transaction records. During the investigation, you may receive provisional credit for the disputed amount. The investigation process usually takes 30-90 days, depending on the complexity of the case and the responsiveness of the merchant.

Preventing Unauthorized ACHMA VISB Charges

Prevention is always better than cure when it comes to unauthorized charges. To protect yourself from fraudulent ACHMA VISB transactions, consider implementing the following security measures:

- Use secure payment methods when shopping online, such as virtual card numbers or payment services that offer buyer protection

- Regularly update your passwords and use strong, unique passwords for each of your accounts

- Monitor your credit report for any signs of unauthorized account openings or suspicious activity

- Be cautious about sharing your card information, even with seemingly legitimate businesses

- Consider setting up transaction alerts with your card issuer to receive notifications of all charges

ACHMA VISB vs. Traditional Credit Card Processing

Understanding the differences between ACHMA VISB bill payments and traditional credit card processing can help you make informed decisions about your payment methods and better understand the transactions on your statement.

Cost Considerations for Merchants

One of the primary reasons merchants use ACHMA VISB processing is the cost advantage compared to traditional credit card processing. ACH transactions typically have lower processing fees, which can result in significant savings for businesses that process large volumes of transactions. These savings may be passed on to consumers in the form of lower prices or special discounts for ACH payments.

However, the cost advantage for merchants sometimes comes with trade-offs in terms of processing speed and dispute resolution. ACH transactions take longer to process than credit card transactions, and the dispute process can be more complex. Understanding these trade-offs can help you appreciate why some merchants prefer ACH processing despite these limitations.

Consumer Protection Differences

While ACHMA VISB transactions processed through Visa's network still offer consumer protections, there are some differences compared to traditional credit card transactions. Credit card transactions typically offer stronger fraud protection and more straightforward dispute processes. With ACH transactions, the dispute process may involve additional steps and longer resolution times.

However, Visa's involvement in ACHMA VISB transactions means that consumers still benefit from many of the protections associated with major credit card networks. This includes the ability to dispute unauthorized charges and the potential for provisional credit during the dispute investigation process.

Processing Speed and Settlement Times

The processing speed of ACHMA VISB transactions differs significantly from traditional credit card processing. While credit card transactions are typically authorized and settled within seconds, ACH transactions are processed in batches at scheduled intervals. This means that ACHMA VISB charges may take 1-3 business days to appear on your statement after the initial transaction.

This delay in processing can affect your available credit and may impact your budgeting if you're not aware of the timing differences. Understanding these processing times can help you better manage your finances and avoid potential overdrafts or credit limit issues.

Best Practices for Dealing with ACHMA VISB Transactions

To effectively manage ACHMA VISB bill payments and ensure a smooth experience with these transactions, consider implementing the following best practices:

Maintain Detailed Purchase Records

Keeping detailed records of your purchases can help you quickly identify and verify ACHMA VISB charges. This includes saving receipts, taking screenshots of online order confirmations, and maintaining a record of subscription services and their billing cycles. When a charge appears on your statement, you can quickly cross-reference it with your records to confirm its legitimacy.

Consider using budgeting apps or spreadsheets to track your purchases and their corresponding payment methods. This organized approach can save you time and frustration when reviewing your statements and identifying legitimate charges.

Understand Merchant Billing Practices

Different merchants have varying billing practices, and understanding these can help you anticipate ACHMA VISB charges. Some merchants may charge your card immediately upon order placement, while others may wait until the item ships. Subscription services may have specific billing cycles that don't align with calendar months.

Take the time to read the terms and conditions when signing up for new services or making significant purchases. Understanding when and how you'll be charged can help you avoid surprises on your statement and better manage your finances.

Communicate with Your Card Issuer

Establishing a good relationship with your card issuer can be beneficial when dealing with ACHMA VISB transactions. Many issuers offer services like transaction alerts, spending analysis, and dedicated customer support for billing inquiries. Take advantage of these services to stay informed about your account activity and quickly address any concerns.

If you frequently encounter ACHMA VISB charges or have specific questions about how these transactions are processed, don't hesitate to contact your card issuer for clarification. They can provide valuable information about their policies and procedures for handling these types of transactions.

The Future of ACHMA VISB and Electronic Payments

The landscape of electronic payments continues to evolve, and ACHMA VISB bill payments are likely to adapt to changing consumer needs and technological advancements. Understanding these trends can help you prepare for future developments in payment processing.

Emerging Payment Technologies

New payment technologies are constantly emerging, from mobile wallets to cryptocurrency transactions. As these technologies mature, they may influence how ACHMA VISB transactions are processed and what information is included in transaction descriptions. The integration of artificial intelligence and machine learning in payment processing may also lead to more detailed and user-friendly transaction information.

Staying informed about these technological developments can help you adapt to changes in how ACHMA VISB charges appear on your statement and what options you have for managing these transactions.

Enhanced Security Measures

As electronic payment fraud becomes more sophisticated, payment processors and card networks are continuously developing enhanced security measures. Future ACHMA VISB transactions may include additional authentication steps, more detailed transaction information, or improved fraud detection capabilities.

These security enhancements may affect how quickly transactions are processed and what information is available for dispute resolution. Being aware of these potential changes can help you adjust your payment management strategies accordingly.

Regulatory Changes and Consumer Protection

Payment processing is subject to various regulations that can change over time. Future regulatory changes may affect how ACHMA VISB transactions are processed, what consumer protections are available, and how disputes are handled. Staying informed about these regulatory developments can help you understand your rights and options when dealing with these transactions.

Consumer advocacy groups and financial regulators often provide updates about changes in payment processing regulations. Following these updates can help you stay informed about any changes that may affect how you manage ACHMA VISB charges.

Conclusion

Understanding ACHMA VISB bill payments is essential for anyone who uses credit cards for retail purchases, subscriptions, or service payments. These transactions, while sometimes confusing due to their cryptic descriptions, represent a legitimate and increasingly common method of electronic payment processing. By familiarizing yourself with how these transactions work, how to identify legitimate charges, and the procedures for managing and disputing them, you can take control of your financial management and avoid potential issues.

Remember that ACHMA VISB charges are typically associated with major retailers like Walmart and Sam's Club, as well as subscription services and utility payments processed through ACH networks with Visa's involvement. Regular statement review, detailed purchase records, and good communication with your card issuer are key strategies for effectively managing these transactions.

As electronic payment technologies continue to evolve, staying informed about changes in processing methods and consumer protections will help you navigate the future of ACHMA VISB bill payments and other electronic transactions. With the right knowledge and proactive management strategies, you can ensure a smooth and secure experience with all your electronic payments.