Is Depreciation An Operating Expense? Understanding The Financial Impact

Have you ever wondered how businesses account for the gradual wear and tear of their valuable assets? When a company purchases expensive equipment, vehicles, or buildings, these assets don't last forever. Their value diminishes over time, and this reduction in value is what we call depreciation. But here's the million-dollar question: is depreciation an operating expense, or is it something else entirely?

This question is crucial for business owners, accountants, and investors alike. Understanding whether depreciation is an operating expense can significantly impact how you view a company's financial health, make investment decisions, or even prepare your own business's financial statements. In this comprehensive guide, we'll dive deep into the world of depreciation, explore its relationship with operating expenses, and help you understand why this distinction matters in the grand scheme of financial reporting and analysis.

What Is Depreciation and How Does It Work?

Depreciation is an accounting method that allocates the cost of a tangible asset over its useful life. Think of it as a way to spread out the expense of a large purchase over several years rather than taking the full hit in one accounting period. For example, if a company buys a delivery truck for $50,000 that's expected to last 5 years, they wouldn't expense the entire $50,000 in year one. Instead, they'd depreciate it, perhaps at $10,000 per year for 5 years.

- Joseph James Deangelo

- Cookie The Monsters Secret Leak Nude Photos That Broke The Internet

- Brett Adcock

The concept of depreciation is based on the matching principle in accounting, which states that expenses should be matched with the revenues they help generate. As assets are used to produce income over multiple periods, their cost should be allocated across those same periods. This provides a more accurate picture of a company's financial performance and helps prevent large, one-time expenses from distorting profit calculations in any single period.

Understanding Operating Expenses

Operating expenses are the costs associated with running a company's core business operations. These are the day-to-day expenses that a business incurs to keep its doors open and generate revenue. Common examples include rent, utilities, salaries, marketing costs, and office supplies. Operating expenses are typically recurring and necessary for the ongoing functioning of the business.

The key characteristic of operating expenses is that they're directly tied to the company's primary revenue-generating activities. If a cost is essential for the company to deliver its products or services to customers, it's likely an operating expense. These expenses are usually recorded on the income statement and are subtracted from revenue to determine operating income or EBIT (Earnings Before Interest and Taxes).

- Will Poulter Movies Archive Leaked Unseen Pornographic Footage Revealed

- Leaked Tianastummys Nude Video Exposes Shocking Secret

- Kaliknockers

Is Depreciation Considered an Operating Expense?

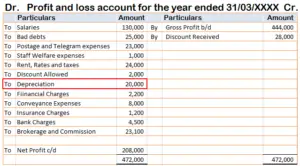

Yes, depreciation is generally considered an operating expense. While it doesn't involve an actual cash outflow, depreciation is classified as an operating expense because it's a cost associated with the company's core operations. The assets being depreciated (like machinery, equipment, or vehicles) are used in the day-to-day running of the business to generate revenue.

Depreciation is typically included in a category called "Selling, General, and Administrative Expenses" (SG&A) on the income statement, which is a subset of operating expenses. This classification makes sense because the assets being depreciated are integral to the company's ability to conduct its business. For instance, a manufacturing company's machinery depreciates as it produces goods, directly linking the depreciation expense to the company's operational activities.

Depreciation vs. Capital Expenditures

It's important to distinguish between depreciation and capital expenditures (CapEx). While depreciation is an operating expense that spreads the cost of an asset over time, capital expenditures are the actual cash outflows used to purchase or upgrade physical assets. When a company buys a new piece of equipment, that purchase is a capital expenditure.

The confusion often arises because depreciation is related to these capital expenditures. However, while CapEx is a cash flow item (appearing on the cash flow statement), depreciation is a non-cash expense (appearing on the income statement). This distinction is crucial for understanding a company's true financial position. A company might show high depreciation expenses, which reduce its reported net income, but this doesn't necessarily reflect its actual cash position or its ability to generate cash from operations.

The Impact of Depreciation on Financial Statements

Depreciation has a significant impact on a company's financial statements, particularly the income statement and the balance sheet. On the income statement, depreciation reduces the company's reported net income, which can affect various financial ratios and metrics that investors and analysts use to evaluate a company's performance.

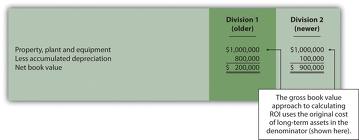

On the balance sheet, depreciation reduces the book value of the company's assets over time. As assets are depreciated, their carrying value (original cost minus accumulated depreciation) decreases. This reduction in asset value is offset by an increase in retained earnings, as depreciation is added back to net income in the equity section of the balance sheet. Understanding this relationship is crucial for accurately assessing a company's financial position and performance.

Depreciation Methods and Their Effects

There are several methods for calculating depreciation, each with its own implications for how depreciation is treated as an operating expense. The most common methods include straight-line depreciation, declining balance depreciation, and units of production depreciation. The choice of method can affect the timing and amount of depreciation expense recognized each year.

For example, straight-line depreciation spreads the cost evenly over the asset's useful life, resulting in a consistent operating expense each year. In contrast, accelerated depreciation methods like declining balance front-load the depreciation expense, recognizing more depreciation in the early years of an asset's life. This can significantly impact a company's reported operating income and, consequently, its tax obligations in different years.

Depreciation in Different Industries

The treatment and significance of depreciation as an operating expense can vary considerably across different industries. Capital-intensive industries like manufacturing, transportation, and telecommunications often have substantial depreciation expenses due to their large investments in long-term assets. For these companies, depreciation can be one of the most significant operating expenses on their income statements.

In contrast, service-based industries or technology companies might have relatively low depreciation expenses, as their primary assets might be intangible (like software or intellectual property) or their physical assets might have shorter useful lives. Understanding how depreciation operates in your specific industry is crucial for accurate financial planning and analysis.

Depreciation and Tax Considerations

While depreciation is treated as an operating expense for financial reporting purposes, its treatment for tax purposes can be different. Many tax authorities allow for accelerated depreciation methods, which can provide tax benefits by reducing taxable income more quickly than financial reporting depreciation. This difference between book depreciation (for financial statements) and tax depreciation is known as a temporary difference.

These tax considerations can significantly impact a company's cash flows and effective tax rate. Companies often engage in tax planning strategies around depreciation to optimize their tax position, which can result in deferred tax liabilities or assets on their balance sheets. Understanding these nuances is crucial for comprehensive financial analysis and strategic decision-making.

Common Misconceptions About Depreciation

One common misconception is that depreciation represents the market value or resale value of an asset. In reality, depreciation is an accounting construct that allocates cost over time and doesn't necessarily reflect the actual value or condition of the asset. Another misconception is that depreciation always results in cash outflows, when in fact it's a non-cash expense.

Some people also mistakenly believe that depreciation is optional or can be ignored in financial analysis. However, depreciation is a required accounting principle under GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards). Ignoring depreciation can lead to significant misstatements in financial reporting and poor business decision-making.

Practical Tips for Managing Depreciation

For business owners and managers, effectively managing depreciation can have significant implications for financial planning and tax strategy. One practical tip is to carefully consider the useful life assigned to assets when calculating depreciation. Estimating a longer useful life can reduce annual depreciation expenses, potentially improving reported profitability.

Another strategy is to take advantage of tax incentives for depreciation, such as bonus depreciation or Section 179 deductions in the United States, which allow for larger depreciation deductions in the year an asset is placed in service. However, it's crucial to balance these tax benefits with the need for accurate financial reporting and to consult with a qualified accountant to ensure compliance with accounting standards and tax regulations.

The Future of Depreciation Accounting

As business models evolve, particularly with the rise of digital assets and subscription-based services, the concept of depreciation is also evolving. The treatment of intangible assets, like software or customer relationships, is becoming increasingly important in financial reporting. Additionally, new accounting standards like ASC 842 for lease accounting are changing how companies account for certain types of assets and related expenses.

Looking ahead, we may see further refinements in how depreciation is calculated and reported, particularly as the line between operating and capital expenses becomes increasingly blurred in the digital economy. Staying informed about these changes is crucial for accurate financial reporting and strategic decision-making.

Conclusion

In conclusion, depreciation is indeed an operating expense, playing a crucial role in how companies report their financial performance and manage their assets. While it's a non-cash expense, depreciation is essential for accurately matching the cost of assets with the revenue they generate over time. Understanding depreciation's treatment as an operating expense is vital for business owners, investors, and financial professionals alike.

By grasping the nuances of depreciation, from its impact on financial statements to its implications for tax planning and industry-specific considerations, you can make more informed decisions about your business or investments. Remember, while depreciation might seem like a complex accounting concept, its practical implications are far-reaching and can significantly impact a company's financial health and strategic direction. As business landscapes continue to evolve, staying informed about depreciation and its treatment will remain a key competency for anyone involved in financial management or analysis.